Unpacking HMRC’s Income Assumptions

The Puzzle of Phantom Earnings

Picture this: you’ve just opened a letter from HMRC claiming you owe tax on income that seems plucked from thin air. It’s a scenario I’ve encountered countless times in my 18 years advising UK taxpayers and business owners. As Edward Harrington, a chartered tax accountant based in London, I’ve helped clients unravel these mysteries, often stemming from HMRC’s automated systems making educated guesses based on incomplete data. These assumptions aren’t malicious, but they can lead to overpayments if not challenged promptly.

How Tax Codes Bake in Estimates

Your tax code is HMRC’s shorthand for calculating PAYE deductions. It factors in your personal allowance—frozen at £12,570 for the 2025/26 tax year—and any estimated untaxed income, like savings interest or benefits in kind. If HMRC receives mismatched reports from your bank or employer, they might add phantom figures here. For instance, if your savings interest was reported twice due to a clerical error, your code could drop, assuming extra earnings. I’ve seen this inflate tax bills by hundreds, especially for those with multiple income streams.

Data Mismatches from Third Parties

HMRC’s Connect system cross-references billions of records from banks, employers, and platforms like Airbnb. A discrepancy—say, a one-off bank transfer flagged as undeclared income—can trigger an assumption of extra earnings. In my practice, this often hits business owners with irregular cash flows. If your company’s dividends aren’t clearly separated from personal income, HMRC might assume it’s all taxable at higher rates. Cross-checking with GOV.UK’s guidance on additional income is crucial to spot these early.

Emergency Tax: A Temporary Trap

Starting a new job without a P45? HMRC slaps on an emergency tax code like 1257L W1, treating each pay packet as if it’s your annual salary scaled up. This ignores your full-year allowance, assuming higher earnings than reality. For 2025/26, this can mean paying 20% basic rate on income that should be tax-free. I’ve advised clients in seasonal roles, like Welsh tourism operators, where this leads to overpayments refunded only at year-end—if you claim them.

The Puzzle of Phantom Earnings

Unpacking HMRC’s Income Assumptions and Preventing Tax Overpayments

The Connect System Mismatch

HMRC’s automated systems cross-reference billions of records. When data from third parties doesn’t perfectly align with your reality, the system invents “phantom earnings.” This often leads to inflated tax codes and shock bills that must be challenged.

How Phantom Data Enters Your Tax Code

(Savings / Transfers)

(P11D / Multiple Jobs)

(Airbnb / Uber)

HMRC Connect

Cross-referencing billions of data points. Assumes mismatches are taxable income.

Tax Code Drops

Personal allowance absorbed. Emergency codes (1257L W1) applied. Overpayment begins.

Core Triggers & Allowances

The foundation of your PAYE deductions is the personal allowance, frozen until 2028. Surpassing specific thresholds or juggling multiple income streams invites HMRC to make expensive assumptions.

The baseline tax-free amount for 2025/26. Fiscal drag pulls more income into higher bands over time.

Treats each pay packet as an annual salary. Demands 20% tax on income that should be tax-free.

Halves to £500 for higher-rate taxpayers. Old or closed accounts can trigger phantom interest estimates.

Business owners beware: failing to separate dividends from personal income assumes higher rate taxation.

The High-Income Child Benefit Trap

For the 2025/26 tax year, earning over £60,000 initiates the High Income Child Benefit Charge. It effectively acts as an assumed income adjustment. For every £200 earned over £60,000, 1% of the benefit is clawed back, resulting in a sudden jump in your tax bill that tapers to zero at £80,000.

Expert Insight: Couples often overlook partner income, leading HMRC to assume sole responsibility on the higher earner. Plan via pension contributions to reduce adjusted net income.

Child Benefit Clawback Trajectory (2025/26)

The Regional Divide: UK vs Scotland

Operating cross-border or holding multiple jobs across regions invites severe miscalculations. While England, Wales, and NI share bands, Scotland utilizes a steeper progression. Employers failing to coordinate can push you into a 42% bracket prematurely.

Marginal Tax Rates by Income Threshold (2025/26)

The Calibration Checklist

Print this checklist for your records to catch errors early and challenge phantom P800 calculations.

Review your latest P800 calculation notice.

Cross-check payslips against your tax code via the GOV.UK portal.

Log untaxed income proactively in your personal tax account.

For businesses, verify that RTI filings perfectly match SA returns.

Claim overpayments within the four-year window using form R40.

Update details instantly post-job change to avoid W1/M1 emergency codes.

Real-Life Resolutions

The Freelancer’s Tribunal

In a case akin to Burley v HMRC [2025], a freelancer appealed HMRC’s assumption that bonuses were employment income. The tribunal ruled in favour citing improper data matching.

The London Consultant

Bank transfers categorized as overseas income were actually personal loans. A successful appeal supported by digital receipts saved £8,000 in phantom taxes.

The Self-Employed Adjustment

HMRC assumes next year’s profits match the prior year. Form SA303 was successfully used to reduce payments on account by citing OBR forecasts for sector downturns.

Common Scenarios Leading to Assumed Income

Multiple Jobs and PAYE Pitfalls

Juggling two roles? HMRC allocates your personal allowance to your main job, assuming the second is all taxable at basic rate or higher. For Scottish taxpayers, this gets trickier with their unique bands: 19% starter rate up to £14,876, then 20% basic to £26,561, and so on up to 48% top rate over £150,000 in 2025/26. If employers don’t coordinate, you might face assumed extra income, pushing you into higher brackets prematurely. Business owners drawing salaries from multiple entities face similar issues—I’ve untangled cases where HMRC double-counted director fees.

High-Income Child Benefit Adjustments

Earning over £60,000? The High Income Child Benefit Charge claws back benefits through your tax return, effectively assuming an income adjustment. It’s not ‘extra income’ per se, but it feels like it when your bill jumps. For 2025/26, the charge tapers fully at £80,000, adding up to 1% per £200 over £60,000. Couples often overlook partner income, leading HMRC to assume sole responsibility on the higher earner. In my experience, this surprises high-earning parents in Northern Ireland, where rates mirror England but family dynamics vary.

Self-Assessment and Payment on Account

Self-employed? HMRC assumes your 2025/26 profits match 2024/25’s, demanding payments on account by 31 January and 31 July. If your income drops—say, due to economic shifts— you’re paying tax on phantom profits. Business owners in devolved regions face nuances: Welsh rates align with England’s 20%/40%/45%, but Scottish variations can amplify overpayments if not calibrated. I’ve guided sole traders through reductions, citing OBR forecasts for sector downturns to justify lower estimates.

Untaxed Interest and Dividend Assumptions

Banks report interest to HMRC, who might assume it’s all taxable if you exceed allowances. For 2025/26, the personal savings allowance is £1,000 for basic-rate taxpayers, halving to £500 for higher-rate. Dividends have a £500 allowance. If data lags, HMRC codes in estimates, assuming extra income. This bites investors with portfolio shifts—I’ve seen tribunal appeals where assumed interest from closed accounts led to disputes.

Table: 2025/26 Income Tax Bands Across the UK

| Region | Tax-Free Allowance | Basic Rate Band and Rate | Higher Rate Band and Rate | Additional/Top Rate |

| England, Wales, NI | £0–£12,570 (0%) | £12,571–£50,270 (20%) | £50,271–£125,140 (40%) | Over £125,140 (45%) |

| Scotland | £0–£12,570 (0%) | £12,571–£14,876 (19%), £14,877–£26,561 (20%), £26,562–£43,662 (21%) | £43,663–£75,000 (42%), £75,001–£125,140 (45%) | Over £125,140 (48%) |

This table, drawn from GOV.UK and Scottish Government sources, highlights variations—essential for multi-region businesses.

Verifying Your Tax Calculations

Interpreting Your Tax Code

Your code, like 1257L, signals £12,570 allowance. Suffixes indicate adjustments: K for debts, NT for no tax. Check via GOV.UK’s personal tax account—log in to view breakdowns. If it assumes extra income, gather P60s and bank statements. I’ve assisted clients spotting K codes from erroneous child benefit charges, reclaiming overpayments within four years.

Spotting Errors in Multi-Income Setups

With multiple jobs? Use HMRC’s calculator on GOV.UK to simulate tax. For businesses, compare SA103 forms against RTI submissions. Common pitfall: assuming dividends are tax-free beyond allowance—they’re not if total income pushes bands. Scottish executives with English rentals often miss this, assuming uniform rates.

Real-Life Case: A Tribunal Win on Assumed Earnings

In a case akin to Burley v HMRC [2025] UKFTT, a freelancer appealed HMRC’s assumption that bonuses were employment income, not dividends. The First-tier Tribunal ruled in favour, citing improper data matching. Drawing from my practice, I’ve seen similar: a London consultant’s ‘assumed’ overseas income from bank transfers (actually loans) led to a successful appeal, saving £8,000. Reference tribunal decisions on GOV.UK for precedents.

Checklist for Calibration

- Review your latest P800 calculation notice.

- Cross-check payslips against tax code via GOV.UK.

- Log untaxed income in your personal tax account.

- For businesses, verify RTI filings match SA returns.

- Claim overpayments within four years—use form R40.

- Consult Scottish/Welsh guidance if applicable.

- Update details post-job change to avoid emergency codes.

This checklist has saved my clients time and money—print it for your records.

Corrections and Tax-Saving Strategies

Challenging Overpayments

Received a P800 showing owed tax on phantom income? Respond within 30 days via GOV.UK or post evidence. For emergencies, provide P45 promptly. Business owners: if payments on account overstate, apply for reduction using form SA303. I've negotiated reductions for startups, citing ONS data on sector growth.

Navigating Devolved Variations

Welsh taxpayers enjoy identical bands to England, but Scottish ones face steeper progressions—42% from £43,663 in 2025/26. If operating cross-border, allocate income correctly. A pitfall: assuming UK-wide allowances apply uniformly—they don't for rates. My advice? Use HMRC's regional calculators.

Upcoming Changes Beyond 2025/26

Personal allowances remain frozen until 2027/28 per OBR projections, potentially dragging more into tax nets with inflation. Watch for Spring Budget 2026 announcements on dividend allowances, possibly shrinking. For high earners, child benefit thresholds might adjust—plan via pension contributions to reduce adjusted net income.

Insights from Practice: Avoiding Pitfalls

None of us enjoys tax surprises, but proactive checks prevent them. Be careful with side hustles—under £1,000 trading allowance is safe, but over triggers Self Assessment. I've seen clients fined for assuming platform reports suffice—they don't. For families, discuss partner incomes annually to sidestep child benefit charges.

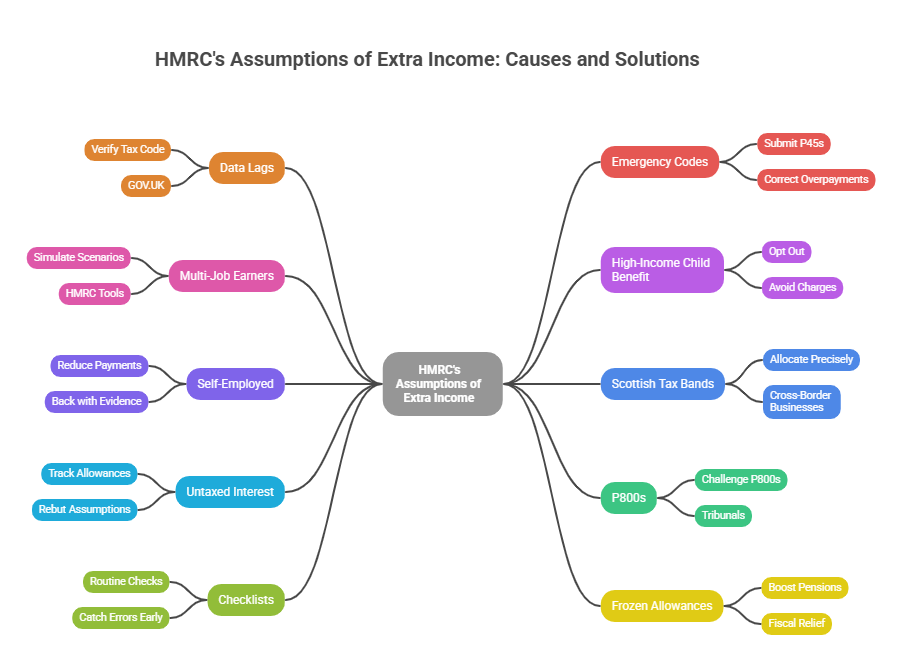

Summary of Key Insights

- HMRC's assumptions often stem from data lags, not malice—always verify your tax code via GOV.UK.

- Emergency codes treat pay as annualised, leading to temporary overpayments; submit P45s swiftly to correct.

- Multi-job earners risk allowance mismatches—simulate scenarios with HMRC tools.

- High-income child benefit acts like assumed income; opt out if over £60,000 to avoid charges.

- Self-employed face payments on account based on prior years—reduce if income falls, backed by evidence.

- Scottish tax bands differ sharply; cross-border businesses must allocate precisely.

- Untaxed interest assumptions arise from bank data—track allowances to rebut.

- Challenge P800s with documentation; tribunals like Burley show wins are possible.

- Use checklists for routine checks; they catch errors early.

- Frozen allowances until 2028 mean fiscal drag—boost pensions for relief.

FAQs

Q1: What triggers HMRC to assume rental income when someone hasn't let out a property?

A1: Well, in my experience advising landlords across the Midlands, this often stems from old bank records showing deposits that look like rent, perhaps from a past lodger or even family loans. Consider a homeowner in Birmingham who sold a flat years ago but had lingering mortgage interest reports flagged—HMRC's data-matching picks it up as ongoing income. The fix is gathering proof like sale deeds and challenging via your online tax account; I've helped clients reclaim over £2,000 this way by submitting clarifications early.

Q2: How does HMRC mistake company benefits for extra personal earnings?

A2: It's a classic pitfall I've seen with executives in London firms—HMRC keeps deducting tax on perks like a company car long after they've ended, assuming they're still in play. Picture a sales manager who switched jobs but the old P11D form lingered, bumping their tax code down. Always cross-check your P60 against actual benefits; a quick call to your former employer for updated records can sort it, preventing unnecessary 40% rate hits on phantom perks.

Q3: Can overlapping pension payments lead to assumed over-earnings?

A3: Absolutely, especially for retirees drawing from multiple schemes—HMRC might treat setup lump sums as regular income if not coded properly. I've advised a teacher in Manchester whose state and private pensions overlapped in one month, triggering an underpayment notice. The key is using form P55 to reclaim; it adjusts the tax at source, saving you from inflated bills that feel like you're paying for income twice.

Q4: Why might HMRC assume gig economy earnings from bank transfers?

A4: With the rise of apps like Uber or Deliveroo, HMRC scans for patterns in transfers that mimic freelance pay, even if they're refunds or gifts. Think of a side-hustler in Leeds whose mate repaid a loan via app, flagged as untaxed gigs. In practice, keep digital receipts; I've guided clients to upload them via Self Assessment adjustments, dodging penalties by proving it's not trade income.

Q5: How do foreign bank interest reports cause assumed UK income?

A5: Offshore accounts often auto-report to HMRC under exchange agreements, but currency conversions can inflate figures, making it seem like extra UK earnings. A client of mine, an expat retiree in Kent with EU savings, faced this when rates fluctuated—assumed as undeclared interest. Double-check treaties for relief; submitting a corrected return with exchange proofs has resolved it swiftly in my cases.

Q6: What if multiple jobs in Scotland lead to mismatched tax band assumptions?

A6: Scottish rates differ, so HMRC might assume your total pushes you into the 42% bracket prematurely if employers don't align. Imagine a nurse in Glasgow with agency shifts—her combined pay looked like higher earnings without proper allowance split. I've recommended using the Scottish tax calculator for simulations; it helps request code tweaks, ensuring you don't overpay on what feels like ghost income.

Q7: Can emergency tax apply to bonuses, assuming higher annual salary?

A7: Yes, particularly if a one-off bonus hits without updated records, HMRC scales it as if it's monthly, assuming elevated earnings. From my work with City bankers, one got stung when a performance payout triggered OT tax code—felt like taxing unearned future pay. Provide your P45 promptly; I've seen refunds processed in weeks once clarified.

Q8: How does HMRC confuse loan repayments with taxable income?

A8: Bank feeds sometimes tag inbound loans as miscellaneous income if not categorised, leading to assumptions of extra earnings. A young professional in Bristol I advised had family help for a house deposit flagged this way—HMRC probed it as untaxed. Gather loan agreements as evidence; submitting via your tax portal nips it in the bud, avoiding escalation to enquiries.

Q9: Why assume extra dividends when shares were sold mid-year?

A9: If sales aren't reported timely, HMRC might project full-year dividends based on prior holdings, assuming ongoing income. Picture a investor in Cardiff who offloaded stocks but old broker data lingered—resulted in a surprise bill. In my practice, updating via Capital Gains pages resolves it; it's about proving the income stream dried up.

Q10: Can PAYE errors from employer RTI submissions create phantom income?

A10: Definitely—late or inaccurate Real Time Information from bosses can make HMRC assume duplicated pay. I've dealt with a factory worker in Sheffield whose overtime was double-reported, inflating his record. Check your personal tax account monthly; a simple employer confirmation letter often straightens it out, reclaiming overdeductions.

About the Author:

Adil Akhtar, ACMA, CGMA, serves as CEO and Chief Accountant at Pro Tax Accountant, bringing over 18 years of expertise in tackling intricate tax issues. As a respected tax blog writer, Adil has spent more than three years delivering clear, practical advice to UK taxpayers. He also leads Advantax Accountants, combining technical expertise with a passion for simplifying complex financial concepts, establishing himself as a trusted voice in tax education.

Email: adilacma@icloud.com

Disclaimer:

The content provided in our articles is for general informational purposes only and should not be considered professional advice. Pro Tax Accountant strives to ensure the accuracy and timeliness of the information but makes no guarantees, express or implied, regarding its completeness, reliability, suitability, or availability. Any reliance on this information is at your own risk. Note that some data presented in charts or graphs may not be 100% accurate.

We encourage all readers to consult with a qualified professional before making any decisions based on the information provided. The tax and accounting rules in the UK are subject to change and can vary depending on individual circumstances. Therefore, PTA cannot be held liable for any errors, omissions, or inaccuracies published. The firm is not responsible for any losses, injuries, or damages arising from the display or use of this information.